Here’s a real example:

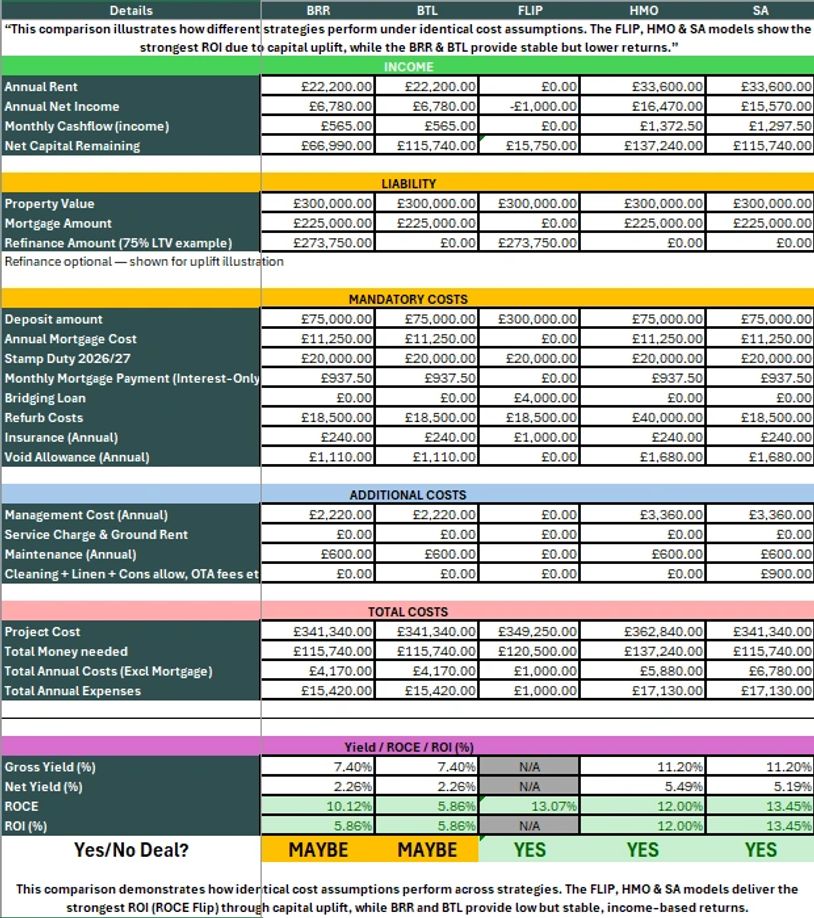

Take this two bedroom house in Juniper, Bracknell RG12 found on Zoopla & Rightmove: Freehold property, currently brought down from £325,000 to £300,000. ROI could be 5.86-13.45% depending on the strategy (ROCE for Flips), making this a possible Flip investment. The property appears to still on the market and the seller may be open to considering a lower offer, creating an opportunity for added value.

Details:

Purchase Price £300,000 - Deposit (if using bridging) 25% =£75,000

Finance Type: Bridging finance (not a mortgage)

Bridging Rate: 0.8%–1% per month (instead of 5% mortgage rate)

Refurbishment Cost: £18,500 (light refurb)

Holding Period: 6–12 months

Other costs: (legal, etc.) £2,000 - Insurance £1,000

Expected Sale Price: £365,000

Property Analysis

This analysis shows the true financial performance of a real Bracknell property using five different investment strategies. It breaks down the cashflow, ROI and total money required so investors can see exactly which approach delivers the strongest returns.

SNAPSHOOT SUMMARY

BRR – Buy, Refurbish, Refinance

- Deposit: £75,000

- Refurb: £18,500

- Annual Cashflow: £6,780

- ROI: 5.86%

- Money Left In After Refinance: £66,990

- Verdict: MAYBE

BTL – Buy to Let

- Deposit: £75,000

- Annual Cashflow: £6,780

- ROI: 5.86%

- Total Money In: £115,740

- Verdict: MAYBE

FLIP

- Total Spend: £120,500

- Expected Resale: £365,000

- Profit: £15,750

- ROCE: 13.07%

- Verdict: YES

HMO – House in Multiple Occupation

- Annual Rent: £33,600

- Annual Cashflow: £16,470

- ROI: 12.00%

- Verdict: YES

SA – Serviced Accommodation

- Annual Rent: £33,600

- Annual Cashflow: £15,570

- ROI: 13.45%

- Verdict: YES

Real example #2:

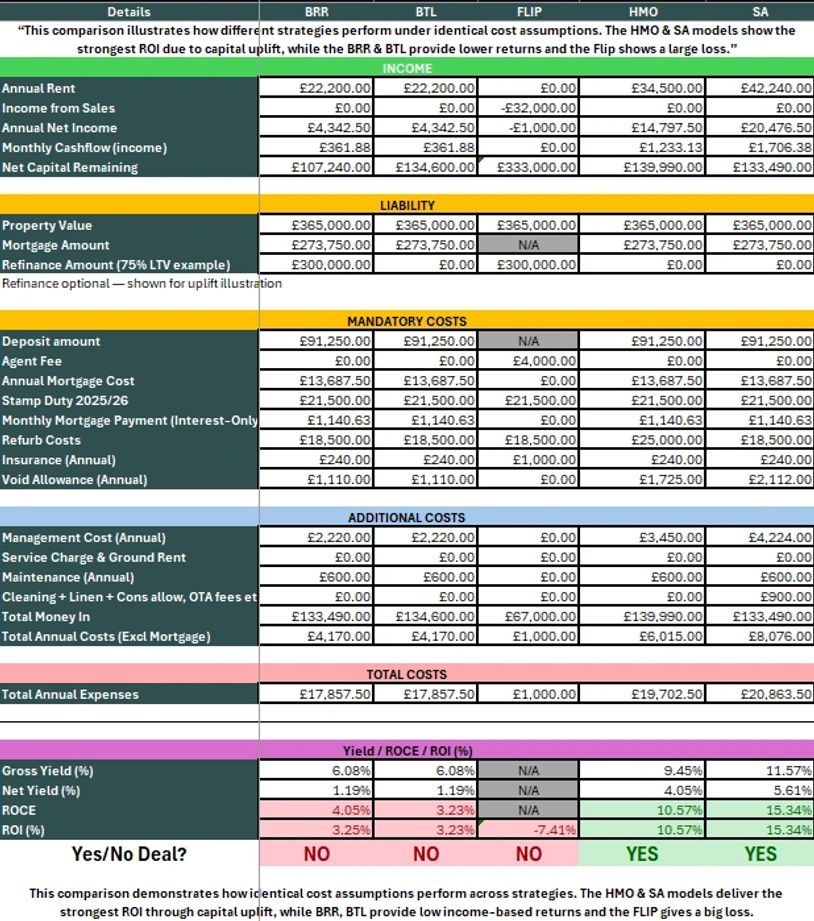

Take this three bedroom house in Bywood, Bracknell RG12 found on RightMove: Freehold property, sold for £365,000. With the correct calculations the ROI would have been 10.15% for a HMO conversion, making this a possible investment.

Details:

Purchase Price £365,000 - Deposit 25% - Mortgage Rate 5% - HMO Rent (pcm) £2,875 - Refurb Cost (Cost per m² list) Light £18,500 (Medium for HMO @ £25,000), Bridging Finance of £20,000 for the HMO - Stamp Duty (2025/26) £21,500. Other Costs (legal, etc.) £2,000 - Management 10% - Maintenance £600 (annual), Insurance £240 (annual) & Void 5%.

Property Analysis

This analysis shows the true financial performance of a real Bracknell property using five different investment strategies. It breaks down the cashflow, ROI and total money required so investors can see exactly which approach delivers the strongest returns.

SNAPSHOOT SUMMARY

BRR – Buy, Refurbish, Refinance

- Deposit: £91,250

- Refurb: £18,500

- Annual Cashflow: £4,343

- ROI: 3.16%

- Money Left In After Refinance: £107,240

- Verdict: NO

BTL – Buy to Let

- Deposit: £91,250

- Annual Cashflow: £4,343

- ROI: 3.16%

- Total Money In: £134,600

- Verdict: NO

FLIP

- Total Spend: £432,000

- Expected Resale: £400,000

- Loss: -£32,000

- ROI: -7.41%

- Verdict: NO

HMO – House in Multiple Occupation

- Annual Rent: £34,500

- Annual Cashflow: £14,798

- ROI: 10.15%

- Verdict: YES

SA – Serviced Accommodation

- Annual Rent: £42,240

- Annual Cashflow: £20,477

- ROI: 15.34%

- Verdict: YES

Property Financial Health Check⭐

Not sure whether your property finances are performing as well as they should? Get a quick, professional review of your income, costs and cashflow - with clear, practical insights from just £25-£85